Download Excel Template

EXCEL (.XLSX)

For: Excel 2007 or later

License: Private Use

What Is Bi-Weekly Mortgage Calculator with Extra Payments?

A Bi-weekly Mortgage Calculator is a tool that uses an amortization schedule where the mortgage payment is done bi-weekly, i.e. every two weeks. A borrower will pay 26 times in a year when repaying their loan.

If someone takes a loan for 30 years in bi-weekly payment frequency, they have to pay their mortgage payment for (26*30)=780 times to repay the loan where both principal and accrued interest will be deducted accordingly every time.

If the borrower’s income increases during the loan repayment period, they might consider an early payoff of the loan, like closing the loan within 25 years by making some extra payments.

What Is Accelerated Bi-weekly Payment?

An accelerated bi-weekly payment is similar to a regular bi-weekly payment as it is also done every two weeks. Here, we assume each month has four weeks. So, to calculate accelerated biweekly payment, monthly payment is calculated with monthly interest rate and all necessary calculations based on monthly payment frequency. The monthly mortgage payment is then divided by two to get the accelerated bi-weekly payment.

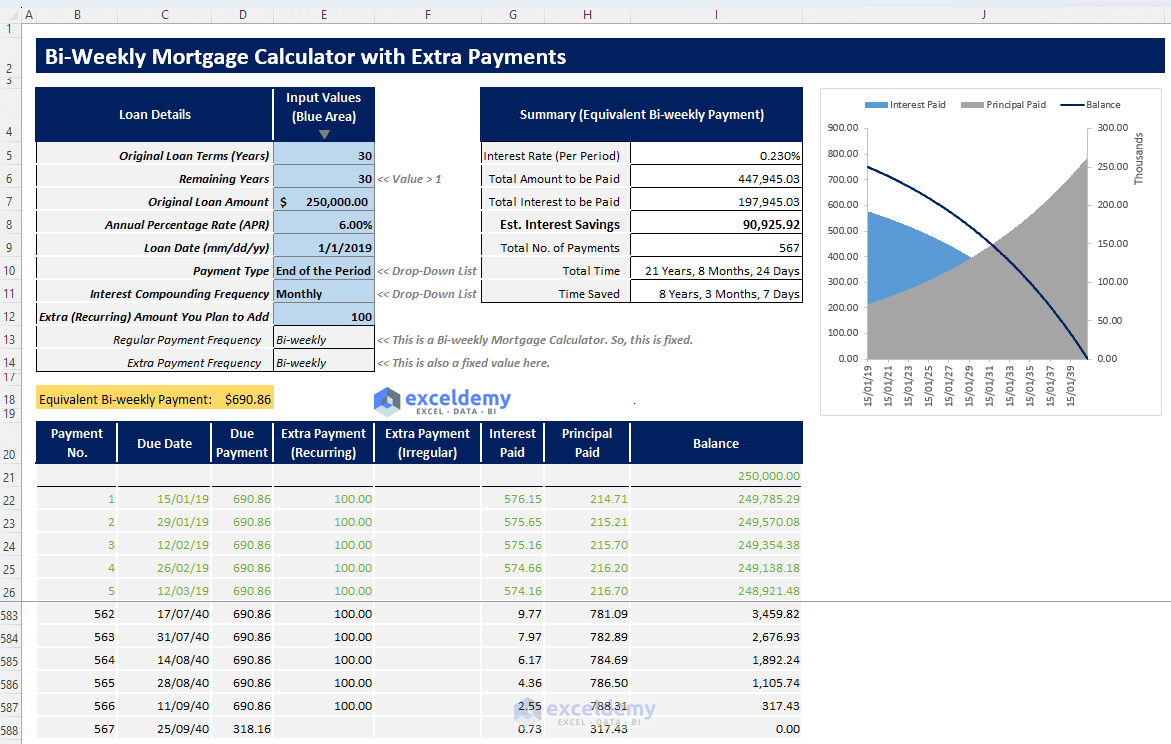

Template 1 – Biweekly Mortgage Calculator with Extra payments

Click to Enlarge Image

This template allows you to input loan details and generate an automated bi-weekly mortgage payment amount with extra payment options. The calculator provides a summary table, amortization table, and a summary chart. These will help you visualize the entire loan repayment process and find all the key output values. It also calculates the potential time and interest savings you can achieve with bi-weekly payments and extra payments compared to a standard bi-weekly payment plan.

How to Use This Template

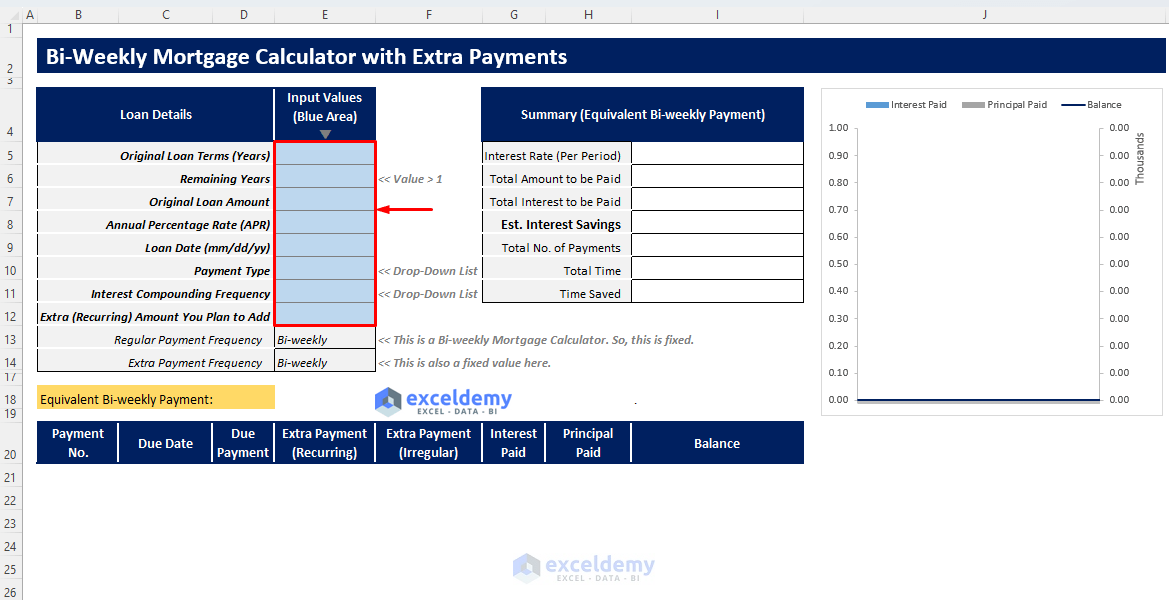

- Open your desired template and insert all necessary inputs in the blue shaded area according to the Loan Details column.

Click to Enlarge the Image

- Since this template is a bi-weekly mortgage calculator, the Regular Payment Frequency is automatically set to bi-weekly. For consistency, the Extra Payment Frequency is also assumed to be bi-weekly.

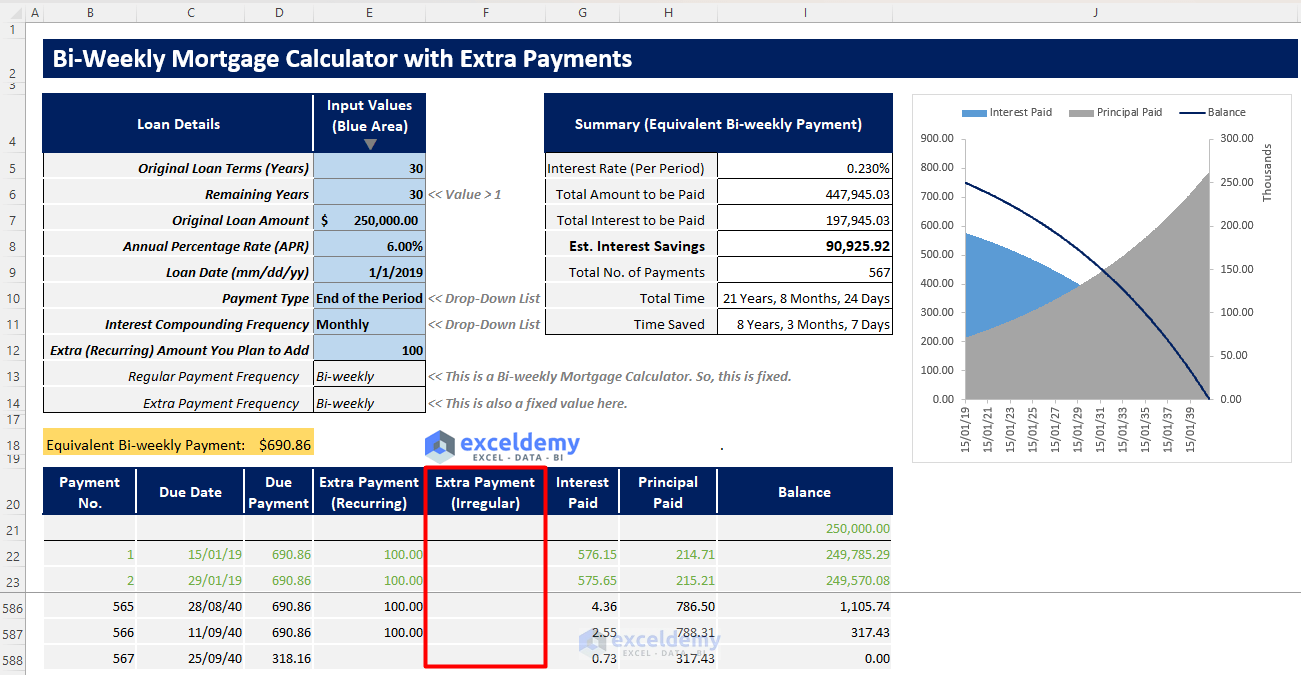

- After entering your loan details, you will see the calculated bi-weekly payment and the following amortization table.

- For unscheduled extra payments, insert them manually in the Extra Payment (Irregular) column of the Amortization table.

Click Here to Enlarge the Image

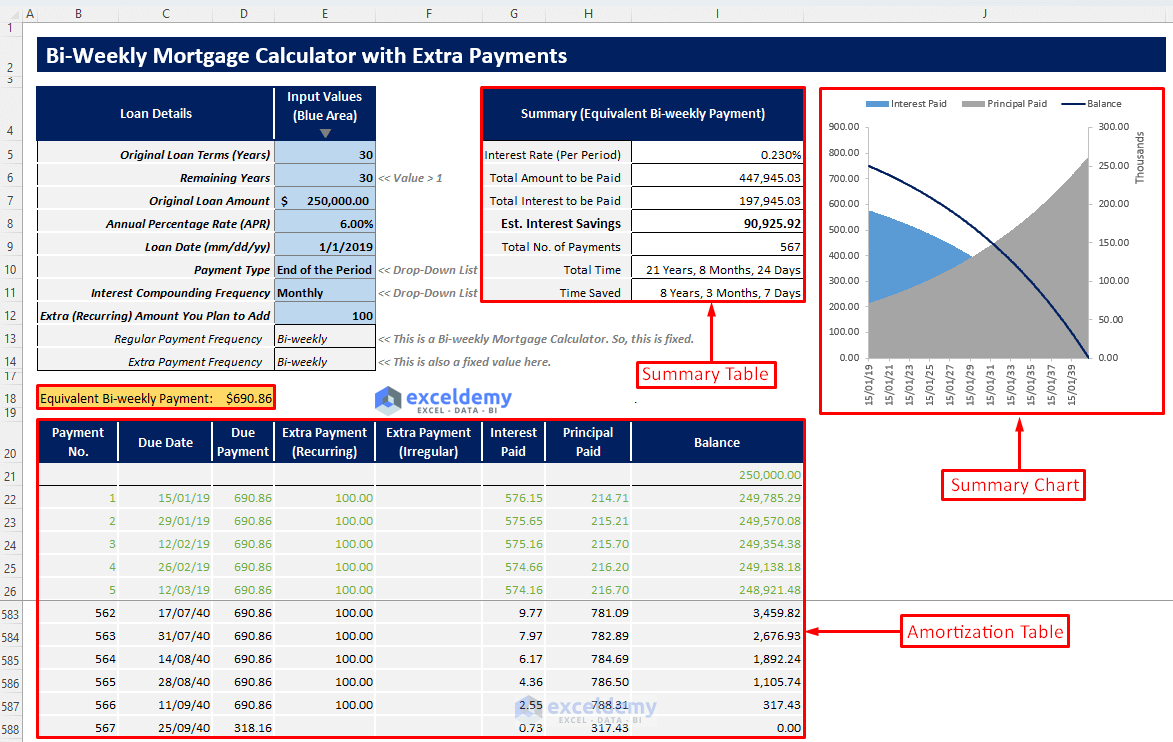

- Once you’ve entered all the information, a summary table will appear. This table displays all the key outputs, including the time and potential interest savings you can achieve with extra payments. You’ll also get the full amortization table, which provides a detailed breakdown of each payment, allowing you to track every transaction throughout the loan term. Additionally, a summary chart offers a visual representation of the mortgage repayment process.

Click to Enlarge the Image

Read More: Mortgage Calculator with Extra Payments and Lump Sum in Excel

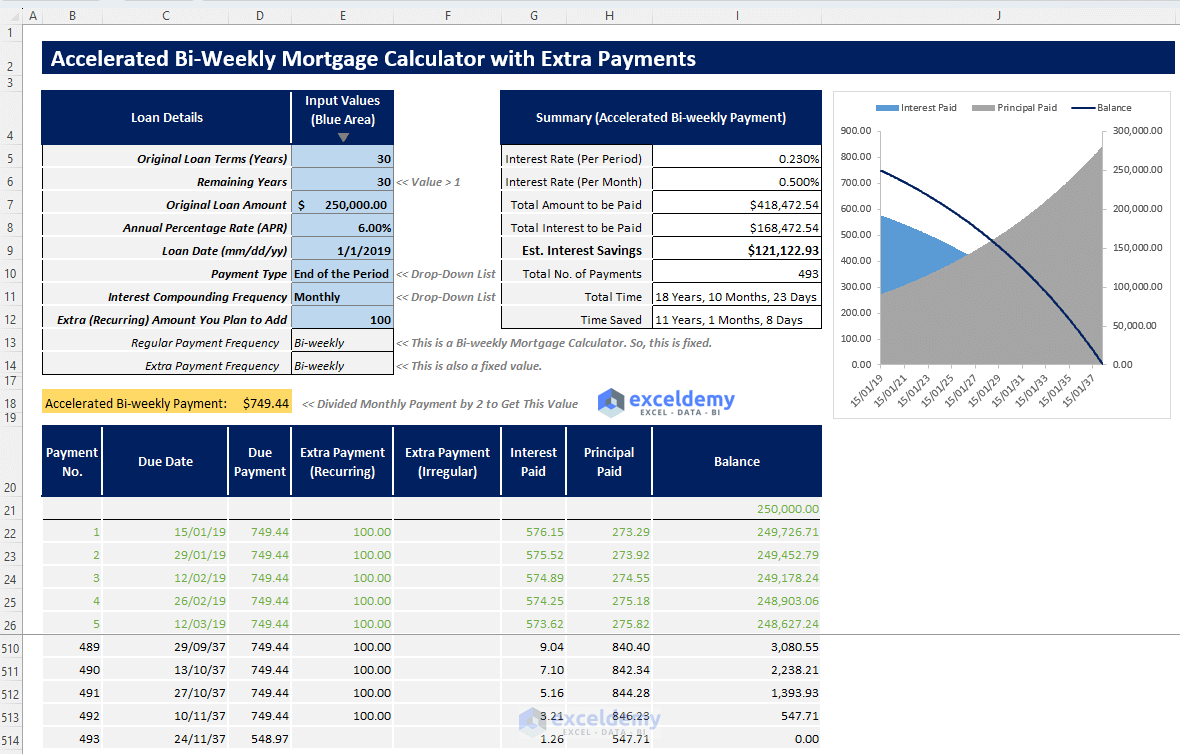

Template 2 – Accelerated Biweekly Payment Mortgage Calculator with Extra Payments

Click to Enlarge the Image

This template will calculate your accelerated bi-weekly payment and will generate an automated accelerated bi-weekly mortgage calculator with extra payments depending on your loan parameters.

Instructions:

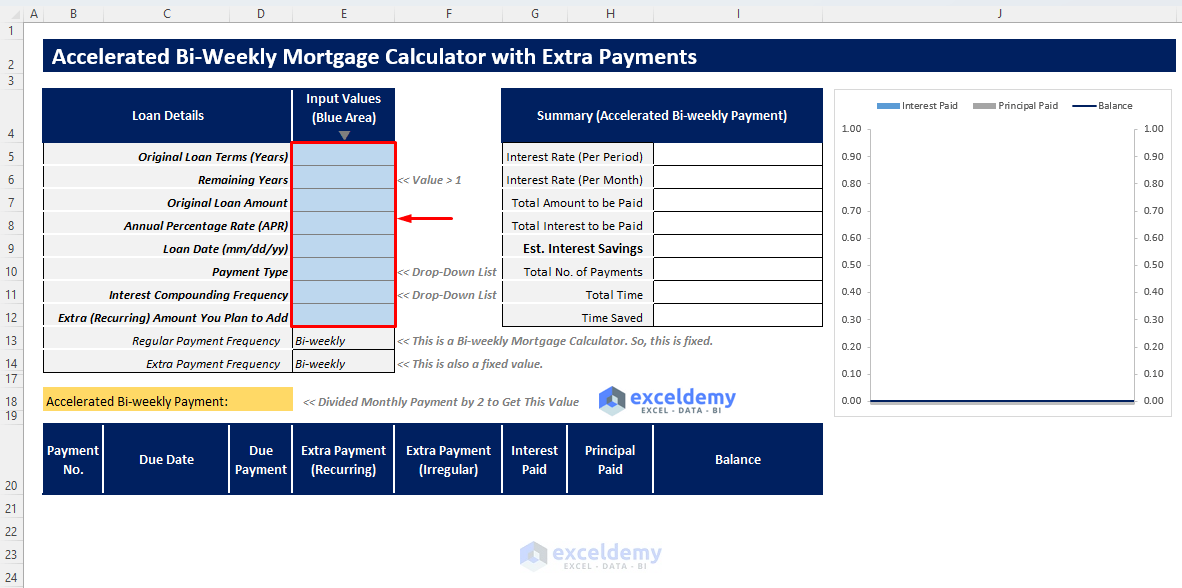

- Open the template and enter the input values in the blue shaded area according to the loan parameters.

Click to Enlarge the Image

- After entering your loan details, you will find your accelerated bi-weekly payment and a summary table along with an amortization table and a summary chart.

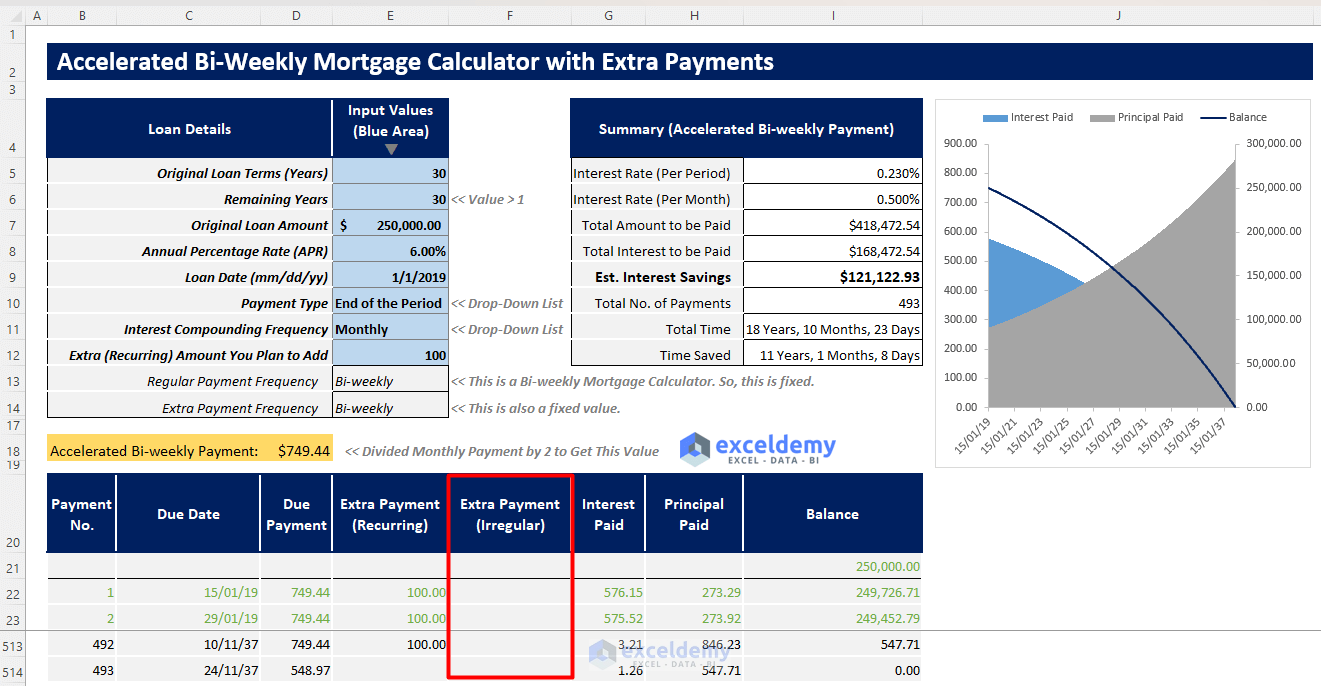

- As this is a bi-weekly mortgage calculator, the Regular Payment Frequency is fixed as a bi-weekly payment. The Extra Payment Frequency is also assumed as a bi-weekly payment frequency here.

- If you have any extra unscheduled payments made or to make, insert them manually in the Extra Payment (Irregular) column of the amortization table.

Click to Enlarge the Image

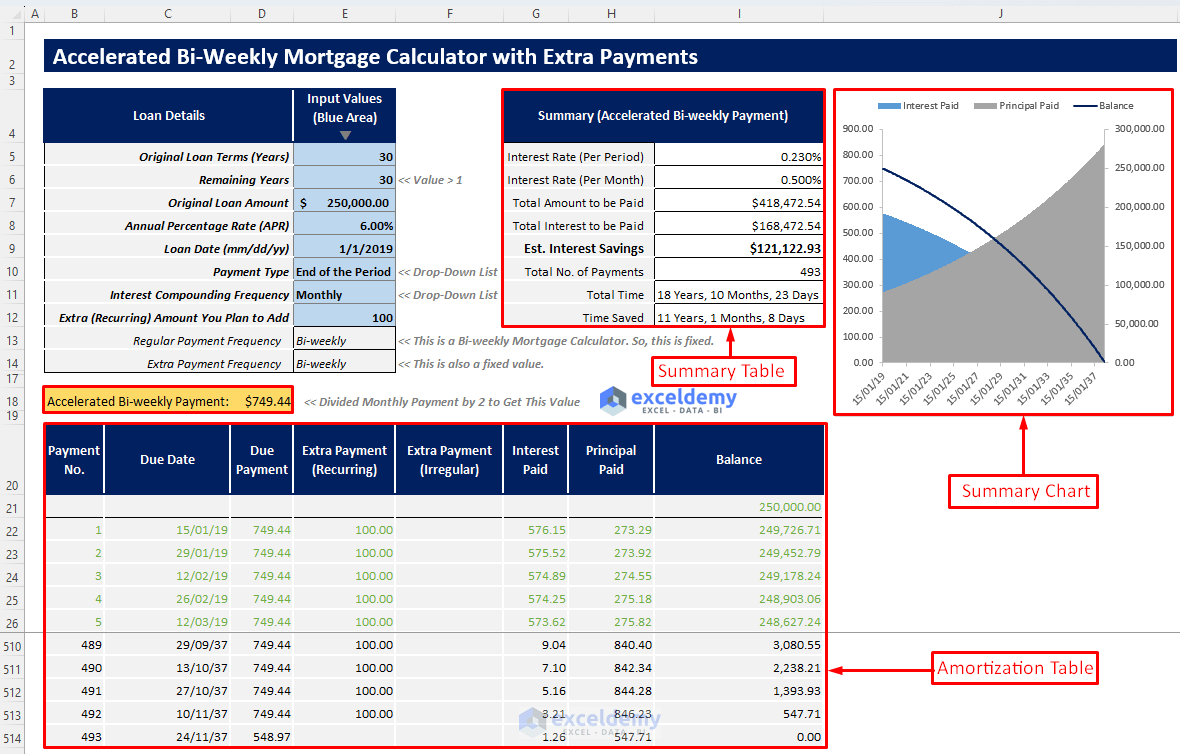

- You will get your summary table containing all necessary outputs along with time saved and estimated interest savings.

- You will also get an amortization table to track your loan repayment and a summary chart to visualize the whole loan repayment process.

Click Here to Enlarge the Image

Read More: Mortgage Repayment Calculator with Offset Account and Extra Payments in Excel

Related Excel Templates

- How to Make Chattel Mortgage Calculator in Excel

- How to Create Reverse Mortgage Calculator in Excel

- Creation of a Mortgage Calculator with Taxes and Insurance in Excel

- Interest Only Mortgage Calculator with Excel Formula

- How to Create Fixed Rate Mortgage Calculator in Excel

- How to Create Offset Mortgage Calculator in Excel

- Early Mortgage Payoff Calculator in Excel

- Calculator for Effective Interest Method of Amortization

<< Go Back to Mortgage Calculator | Finance Template | Excel Templates

can’t open file in Office 365. Error message states; “This file is corrupted.”

Hi Denny,

I am using Microsoft 365 (Home) and it is working on my side perfectly. Please try again.

Thanks.

How can you adjust for missed payments?

This is not completely automatic, Lea!

How do you revise for missed payments?

This is not completely automatic, Lea!

Kawser, how do I contact you directly?

Hello, Kim! You can contact him through this email address:

[email protected]

Hi – I love what you built here…. thank you. Ive been trying to use your calculator and can never get the math quite right and I realized why. Its because in your formula, I am literally paying every 2 weeks, however Im with Chase, and they just hold my first payment, and dont apply it till they receive my second payment. Ive tried hacking what you build but I break it every time. Any chance you can show me a version where the bank only receives my money every 4 weeks, not every 2. Thanks in advance. -Jon

Hey there, Thanks for sharing your problem here. Try the following excel worksheet in the article

https://www.exceldemy.com/mortgage-calculator-with-extra-payments-and-lump-sum-excel/

and try to solve the issue with this excel template. and make sure to follow the instructions mentioned in the article.

If you have any queries regarding excel, feel free to share. Also, you can post your Excel-related problems in the ExcelDemy Forum (https://exceldemy.com/forum/) with images or Excel workbooks.

Regards

Exceldemy Team

Thank you this was very helpful and user friendly!!!

Hello Jennifer,

You are most welcome.

Regards

ExcelDemy

Many errors in DATE DUE field – not editable w/o password. Moving on.

Hello Jennifer,

Thank you for your feedback. Our template auto-calculates the “DATE DUE” field based on your inputs, ensuring accuracy and efficiency. All input fields are editable, and no password is required.

We just freeze the row-20 two maintain the template dashboard.

To unfreeze it select row-20 >> from View >> select Unfreeze Panes.

Please check our how to use this template section carefully.

If you encounter specific issues, please share the details, including screenshots, so we can assist you better. We are committed to resolving any problems you may face.

Regards

ExcelDemy

Hi

When entering a value for Remaining Years it doesn’t compute Extra (Recurring) Amount You Plan to Add

For example,

Original Loan Terms (Years) 30

Remaining Years 27

Extra (Recurring) Amount You Plan to Add 50

When entering these values the Extra Payment (Recurring) Column doesn’t display the recurring amount or calculate the interest savings

Hello Anthony,

Hi, thanks for checking this. The file is working as intended. When Remaining Years is less than the original loan term, the calculator applies the recurring extra payment only to the remaining amortization period and calculates interest savings relative to the remaining balance, not the original 30-year schedule.

Because interest that has already accrued cannot be saved, the impact of a smaller extra amount (like 50) may appear limited when fewer years remain, even though the extra payment logic is being applied correctly.

So this behavior is expected and not a formula error in the Excel file.

Regards,

ExcelDemy